Please use this form if you are applying for the Investment Loan Leverage Strategy.

PERSONAL INFORMATION

EMPLOYMENT AND NET WORTH

BENEFICIARIES

INVESTOR PROFILE QUESTIONS

The questions in this investor profile questionnaire were designed to help you understand your investment objectives and your investment personality. You may use this service to support your investment-making decision or to select an allocation tailored to your needs. As you answer the following questions, remember there is no right or wrong answer. However, keep in mind that you must be completely candid, or the results won’t reflect your true investment personality. Please answer each question and find your score in the box next to each answer. Your total score will help you define your investment profile. If you have more than one account, please consider filling out one questionnaire for each account. Each account you hold may have a different purpose, which may affect your investment decisions.

INVESTMENT HORIZON

REASON WHY WE ARE RECOMMENDING THIS STRATEGY

The applicant would like to invest their money where they could potentially see a larger gain than traditional methods. Because of this we recommended the borrow to invest strategy and have explained all risks involved. The applicant has agreed that this route is one that fits their investment goals. We will invest the funds according to their investor profile.

ADVANTAGES OF WORKING WITH US

SIMPLICITY

With your advisor, you can determine which portfolio best suits your needs based on your investor profile.

You need not worry about choosing funds within the portfolio; these are selected by the portfolio manager based on the markets and their economic outlook.

Periodic review to maintain the allocation of your investment portfolio and in keeping with your risk tolerance.

EFFECTIVENESS

Growth with less volatility, thanks to a diversification of asset classes, managers, management style, geographies and economic sectors.

Access to multiple quality funds.

Expertise of renowned fund managers

LEVERAGE LOAN DISCLOSURE

ACKNOWLEDGEMENT AND REVIEW OF THE BORROWING-TO-INVEST INFORMATION

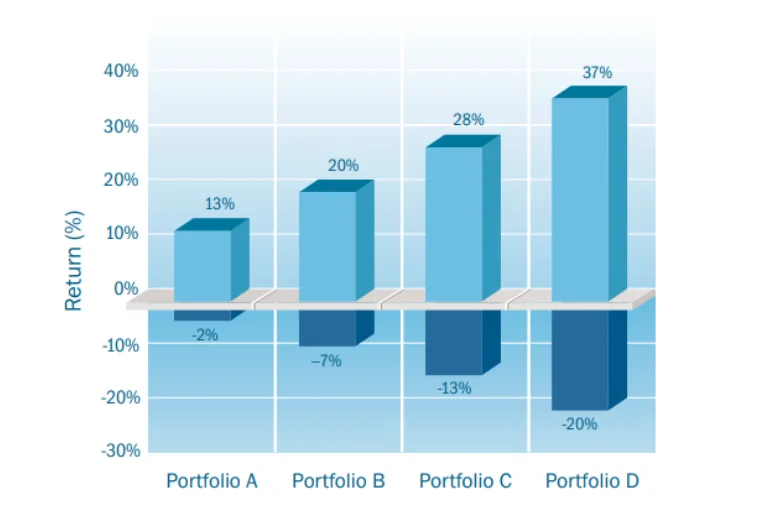

Borrowing to invest uses money from a loan to acquire investments. The primary benefit of this strategy is to provide investors with the potential to increase investment gains. The primary risk is that any investment losses will also be magnified.

Borrowing to invest can be an effective alternative to a regular investment program when used in the right situation. It may be appropriate when your circumstances meet a number of conditions, such as if you have:

A high marginal tax rate

Available and reliable cash flow

Little or no debt

Adequate time horizon (must be considered a long-term strategy)

Comfort with a high level of risk

Strong investment knowledge and experience

High net-worth - ability to handle unplanned financial situations

Borrowing to invest is not a suitable strategy for everyone. Before deciding upon this path, you must fully understand and be completely comfortable with the risks, and have a realistic expectation of the potential benefits.

POTENTIAL RISKS

Market volatility may result in poor investment returns. You may end up owing more on the loan than the investments are worth. The loan, principal plus interest, still must be paid, and you may have to do so from your own resources.

Affordability of the loan payments could be affected by either:

An increase in interest rates; or,

A decrease in your personal income.

The lender could require additional assets be pledged as collateral if the value of the investment drops below the balance of the loan.

POTENTIAL BENEFITS

Investing an initial lump sum creates greater potential for compound growth compared to making smaller regular investment purchases.

The interest expense related to the investment loan may be tax-deductible.

THE INVESTMENT LOAN

The loan used as part of a borrowing-to-invest strategy can take many forms, including a:

Personal line of credit;

Demand loan with a variable interest rate;

Term loan with an interest rate fixed for a specific term; or,

Home equity line of credit or mortgage.

Depending on the type of loan used as part of the borrowing-to-invest strategy, the lender may require you to pledge assets as collateral. These assets would often include the investments purchased with the loan or other assets, such as your house.

For the borrowing-to-invest strategy to succeed, the investments must earn sufficient income to cover all costs, including interest on the loan, fees and other expenses. As interest rates rise, the risk that the investments may not cover all expenses also increases.

INVESTMENT PORTFOLIO

When investing the proceeds from an investment loan, consider these points:

Ensure you have an overall asset mix that is suitable for your situation.

The investment should have the realistic ability to achieve returns that will cover or exceed expenses.

TAX CONSIDERATIONS

Interest will generally be tax deductible if the loan proceeds are used to acquire an investment from which the purchaser has a reasonable expectation, at the time of purchase,

of receiving income.

If some of the investments acquired with borrowed money are redeemed and the proceeds used for personal purposes, the amount of interest expense that is tax deductible will also be reduced proportionally by the amount of the investments redeemed.

For the purposes of interest deductibility under the Income Tax Act (Canada), capital gains are not considered to be income. However, the Canada Revenue Agency (CRA) has indicated in a number of its policy documents that it generally considers the purchaser of an investment fund to have a reasonable expectation of receiving income. While the CRA has been consistent in its assessing practices relating to interest deductibility, there is no guarantee that either the law or CRA assessing practices will not change in the future. For clarification, speak to a tax professional.

Borrowing to invest can create a cumulative net investment loss (CNIL) balance. This may affect your ability to claim a capital gains exemption in respect of qualified small business corporation shares or qualified farm property. If you own property of either type, you should seek advice from a professional accountant before considering a borrowing-to-invest strategy.

IMPLEMENTATION

Your advisor can provide direction and assistance to help you implement a borrowing-to-invest strategy or answer any additional questions you may have. It is important to review any adopted financial security planning strategy with your advisor on a regular basis.

ACKNOWLEDGEMENT AND REVIEW OF THE BORROWING-TO-INVEST INFORMATION

I have read the above and am aware that borrowing to invest can increase gains and losses, and that if my investments go down in value I still have to repay the full loan amount, which may have to come from my personal resources. I understand and accept the potential risks of borrowing to invest.

I hereby irrevocably authorize my advisor to:

(i) limit my exposure to high-risk funds to no more than 50 per cent of the value of my policy at any given time; and

(ii) redeem units of high-risk funds to approximate the 25 per cent target and allocate the amount redeemed to units to another segregated fund of my Advisor and/or its Associates and Partners.

My Advisor and/or their Associates, Agents, Partners and employees will notify me of any redemption and allocation. My Advisor and/or their Associates, Agents, Partners and employees may act or not act on my direction as and when it, in its sole discretion, chooses to do so. I hereby indemnify my Advisor and/or their Associates, Agents, Partners and employees, against any and all costs, damages and liability of any kind relating to their actions or inactions with respect to this authorization and direction, and specifically for allowing my policy to exceed the 25 per cent target or the allocation of assets to lower risk fund(s).

"High-risk" funds are identified as such on applicable Fund Facts. The risk level of a fund can change from time to time, and funds may be added or removed from the high-risk fund list. I can obtain a copy of the current list from my advisor. I understand and agree that the forgoing forms part of my relationship with my Advisor and/or their Associates, Agents, Partners and employees. In the event of a conflict between the terms of this authorization and direction and any other provisions of my contract with my Advisor and/or their Associates, Agents, Partners and employees, this provision shall take precedence.

REASON WHY WE ARE RECOMMENDING THIS STRATEGY

The applicant would like to invest their money where they could potentially see a larger gain than traditional methods. Because of this we recommended the borrow to invest strategy and have explained all risks involved. The applicant has agreed that this route is one that fits their investment goals. We will invest the funds according

to their investor profile.

ACKNOWLEDGEMENT

I hereby acknowledge that the above investment risk stance is consistent with my investment risk requirements and profile. Before making any investment decision, I will fully understand the product risks and features in order to determine that my investment decision is consistent with my investment objectives, risk-appetite and financial resources.